Punishment alone is not a punishment for a healthy and sustainable industry environment.

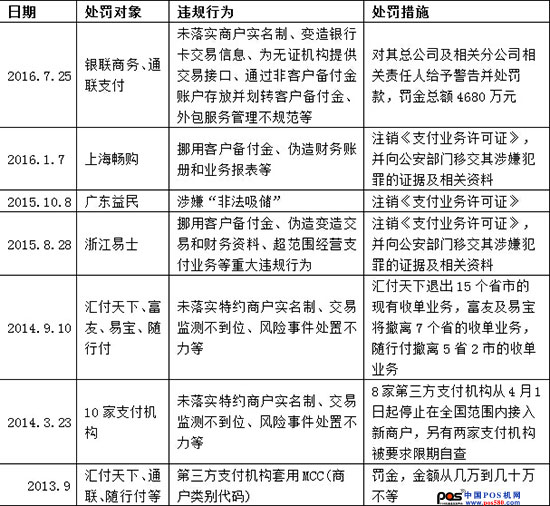

Recently, the central bank issued a huge amount of 46.806 million yuan to UnionPay Business and Tonglian, causing widespread concern in the industry. In recent years, the field of payment and liquidation has become a mess, attracting the central bank to repeatedly make heavy efforts. From August 2015 to January 2016, the central bank successively revoked the “Payment Business Permit†of Zhejiang Yi Shi, Guangdong Yimin and Shanghai Changchun. In May 2016, the first batch of 27 licensees was postponed. The renewal of the license plate, this time opened the largest ticket in history.

Experience tells us that behind the industry chaos, it often involves industry reasons. The violations are only appearances, and the essence behind the appearance is not seen. Punishment alone is not a healthy and sustainable industry environment. After all, who wants to be old and step on the red line to play. Therefore, in this article, the author focuses on the secret behind the violations in the payment and clearing industry, to see what is the cure.

Industry chaos, people are eye-opening

Let’s take a look at why UnionPay’s business and communications are penalized. The reasons given by the central bank are:

"After verification, the above two companies have unimplemented real-name system of merchants, changed bank card transaction information, provided trading interfaces for unlicensed institutions, deposited and transferred customer deposits through non-customer reserve accounts, and outsourced service management is not standardized. When serious violations occur, the report is basically true."

The author has sorted out several penalties imposed by the central bank on the payment industry in recent years. See the following figure, and found that the main violations are concentrated in the bank card acquiring business, which is represented by the unrealized account real name system, providing trading interfaces for unlicensed institutions, and misappropriation. Customer reserve funds, forged transaction materials, package codes, etc. A careful analysis of these violations is really eye-opening.

Source: Suning Financial Research Institute organized from the network

Chaos 1: The flood of "two clears"

Let's first talk about the provision of trading interfaces for unlicensed institutions and the management of outsourcing services. These two problems are mainly manifested as one problem, namely, two clear. The so-called Erqing, simply can be understood as a third-party agent between the payment institution and the merchant. The original transaction funds are directly liquidated to the merchant. Under this model, the transaction funds are first liquidated to the agent (ie Erqing). Then liquidate to the merchant.

In many cases, Erqing will also develop Sanqing, Siqing and even Wuqing downwards, which will make the trading links one-stop, the transaction funds will be transferred layer by layer, and the trading background is complicated.

Through the second Qing, the payment institution can quickly expand the size of the special merchants, which is a powerful weapon to occupy the market share. Obviously, the positive effect is there. However, in recent years, the negative impact has far exceeded the positive significance.

The main hazards of the Erqing business model are twofold:

First, the safety of merchants' funds is endangered. Once the Qingqing institutions (or Sanqing and Siqing) have difficulties in cash flow, debt disputes, and even the running of funds, it is difficult to guarantee the merchant funds. In recent years, there have been a number of incidents in which the second-institutions have been running on the funds, causing collective complaints and disputes from merchants to payment institutions;

Second, if outsourcing management is not in place, it is easy to violate the anti-money laundering regulations and step on the red line of money laundering.

Chaos 2: Set of codes prevails

Let's talk about the set of codes. The so-called set code, that is, the violation of the business category code (MCC) of the low-rate industry, is one of the most common violations of the acquiring business. Different MCC codes represent different industries, and the card processing fee rates are different. According to the newly revised rate regulations of the “No. 66 Document†of the National Development and Reform Commission on February 25, 2013, “5812†represents a restaurant with a handling rate of 1.25%; “5311†represents a department store with a handling rate of 0.78%; “5411†represents In the supermarket, the handling rate is 0.38%, the “three rural†business is lower, and the lowest one is only 0.25%. Obviously, the restaurant can use the MCC code of Sannong to significantly reduce the credit card rate.

There are four main methods for nesting:

The first is to directly falsify false merchant information, including forging business licenses and merchants' access materials, and directly disguising high-rate merchants as low-rate merchants;

The second is to apply for a business license for low-cost industries in batches;

The third is to cut the machine, that is, some acquirers forcibly change the merchants of other acquirers into their own merchants in the name of upgrading the POS machine, implement the set-up behavior in the process of cutting the machine, and reduce the merchant rate to obtain the cooperation of the merchants;

The fourth is platform-based and intelligent fraud, that is, the acquiring institution combines multiple sets of transaction information for the same transaction by changing the transaction type or trading channel, and charges in batches at a low rate of “special billingâ€.

In March 2014, eight acquiring institutions such as Remittance and Epro were ordered by the central bank to suspend access to new merchants, and in September of that year, they requested to withdraw from specific regional businesses, providing opportunities for some of the “cutting machine†behaviors of acquiring companies. . These institutions use the reduced rate to bait, induce the merchants of the penalized institutions to "upgrade" the pos machine, and take the customers back to their own.

There are two main hazards of the nesting code:

First, it disrupts the normal market order. Some acquirers attract merchants through the package, and squeeze the living space of the compliance and operation of the acquirer;

Second, in the process of implementing the parcel behavior, it will inevitably involve counterfeiting merchant information, changing transaction types and other irregularities, making the various risk control measures of the bank card acquiring business ineffective, increasing the risk of money laundering and fraud.

Chaos 3: serious violations such as money laundering and fraud

If the second Qing and the set code are to some extent the vicious competition behavior of the acquiring company in order to increase market share, money laundering, fraud and other acts are suspected of criminal offences. At this point, the acquiring company is no longer subjectively bigger and stronger, but ran and ran, and the motivation has undergone fundamental changes. Generally speaking, money laundering, fraud, etc. are often accompanied by unrealized merchant real-name system, misappropriation of customer reserve funds, retention, theft or disclosure of bank card sensitive information and other high-risk behaviors.

The unimplemented real-name system of merchants is basically the precondition for illegal activities such as set-up, money laundering, etc. Retaining, stealing or leaking bank card sensitive information itself is suspected of fraud, which is a serious violation. Needless to say, the misappropriation of customer reserve funds, there is no technical content, there is courage, it is a serious violation, the three payment agencies that have been canceled licenses are stepping on this red line. Therefore, if the practitioner is a normal brain, no matter how profitable, he will not step on this red line.

Why is the violation operation? Behind the deep geometry

Money laundering, fraud and other acts belong to the motive of paying enterprises. There is nothing to say about strictness, heavy punishment, or even cancellation of licenses and criminal responsibility. Erqing and set code are essentially a kind of competitive means. Although the risk incidents are frequent and the punishments are repeated but repeated prohibitions, there are deep-seated reasons behind them, which cannot be generalized.

Let's take a look at how many of these violations are. China UnionPay Business Management Committee has issued a “Notice on the Standardization of Bank Card Acceptance Markets in the First Half of 2014â€, referring to “In the first half of this year, the country confirmed 460,000 illegal merchants, accounting for 5.84% of the active merchants. Merchants accounted for 77.03%, and bank-infringed merchants accounted for 22.97%. From the perspective of violations, the coded behavior accounted for 39.68%, which is the main problem of market violations."

What is the violation? The fee for swiping is low, and it is the root cause that the acquiring company is difficult to make a profit. The president of UnionPay, Wen Zhaochao once pointed out that most of China’s problems are in the pricing mechanism, which leads to the distortion of behavior of all economic entities.

In fact, due to the low rate of domestic bank card swiping fees, UnionPay has been accused by international card organizations of vicious price and abnormal competition. The problem is that the pricing party is not a UnionPay but a Development and Reform Commission. In 2013, the National Development and Reform Commission issued a document to reduce the commission rate to 6-8 percent. According to this rate, under the 7:2:1 revenue sharing mechanism, the acquirer that relies only on 20% of the card processing fee is basically not making money. .

Under the industry's meager profit mode, doing large-scale is the only means of living. However, in the offline acquiring market, UnionPay business and banks account for about 80% of the market share, and more than 60 licensed acquirers compete for less than 20% of the market, which is itself a competition in the Red Sea.

Looking at the competitor's mentality, the bank side intends to obtain merchant deposits, does not expect the acquiring business to make money, and can't wait for zero expenses to expand merchants; large third-party payment companies do not expect to rely on the acquiring business for profit, intended to pass Single business obtains merchant information, deposits funds, and conducts other Internet finance businesses, and then takes money from VC.

In the case that the level of fees is already low, in the face of competitors who have to pay for hate, most small and medium-sized acquiring institutions rely on legitimate competition means to survive, and they have to take risks and cause the industry to become chaotic and the atmosphere is worse.

Of course, this is not a matter of ethos in nature, but an imbalance between the pricing mechanism and the distribution mechanism of benefits. If you don't solve this problem, and then severely punished, I am afraid that the industry will not be able to stop.

What is the situation next? What I can do is just wait

In March of this year, the National Development and Reform Commission issued the "Notice on Improving the Pricing Mechanism for Bank Cards and Fees", proposing that "the service fee for the collection of the link will be subject to market adjustment. The charge for the collection of services received by the acquirer will be changed from the current government guidance price to the implementation of the market. Adjust the price, and the acquirer and the merchant negotiate to determine the specific rate."

Has the problem been solved? I am afraid not.

So many competitors can't wait to zero-expansion to expand merchants. The market-based pricing is not necessarily the improvement of the overall charging level, but more likely the further reduction of the charging level. The downward adjustment will further reduce the living space of small and medium-sized acquiring institutions, forcing them to continue to take risks and fall into a vicious circle.

How to do it? Forcing everyone to raise the rate is to increase the profit margin for small and medium-sized acquirers? Obviously neither realistic nor reasonable.

The only thing that can be done is that it can only wait for the market to clear. With the gradual withdrawal of the participants, the market will gradually reach a balance, and the soil of chaos will naturally not exist. Is there a way to speed up this process? It is probably the most effective way to use the cancellation of the licence as a means of punishment.

Product details

Cleaning up after your pet is easy with the convenience and dependability of OUT! PetCare Pick-Up Bags.

LEAK-PROOF BAGS: The leak-proof design of OUT! PetCare poop bags allows for ease of mind while picking up dog poop. No worries about any unpleasant surprises leaking out of the bag.

STRONG, DURABLE SUPPORT: The dependable, strong design of OUT! PetCare poop bags means you never have to worry about the process of picking up poop at home or out and about.

FUN, NEW PATTERNS: The new colors and designs on the bags makes cleaning up after your dog easy and stylish while on a walk or even just in your backyard.

SIMPLE CLEANUP: The 9x12 size allows for plenty of room to clean up after your dog.

DOG BAG DISPENSER COMPATIBLE: These fashion dog poop bags fit all OUT! PetCare dispensers as well any dispenser that holds standard dog poop bag rolls.

Three-Dimensional Bags,Plastic Three-Dimensional Dog Poop Bags,Plastic Three-Dimensional Pet Waste Bags,Plastic Three-Dimensional Bags

Taizhou Jinchi Sanitary Product Co., Ltd , https://www.petwastebagtzjc.com