Is the POS less than 0.6% rate? Can you brush? Tell everyone about it now.

Nowadays, all kinds of "brushes" on the market can be said to be flooding, all kinds of free delivery, and various rates, and whether there is any "catty"

I don't know if you have heard that you can't brush a POS machine with a rate lower than 0.6%. Do you know why?

If you want to understand the system and want to be an expert and don't be fooled, please take a few minutes to read it.

First, popularize some simple basics:

Do you have such an experience: You go to spend, when you check out, the clerk will tell you in a vague way, "Today the POS machine is just broken, so please pay cash." Why? Because you swipe your card, the merchant has to pay a certain percentage of the fee. For example: You have dinner today, spending 1,000 yuan in the hotel. But in fact, the business is not able to get 1,000 yuan. The merchant got 994 yuan and paid a 6 yuan handling fee.

This is one of the reasons why some merchants will ask customers to charge a fee.

Where is the so-called "handling fee"? They are collected by the issuing bank, UnionPay and acquirer.

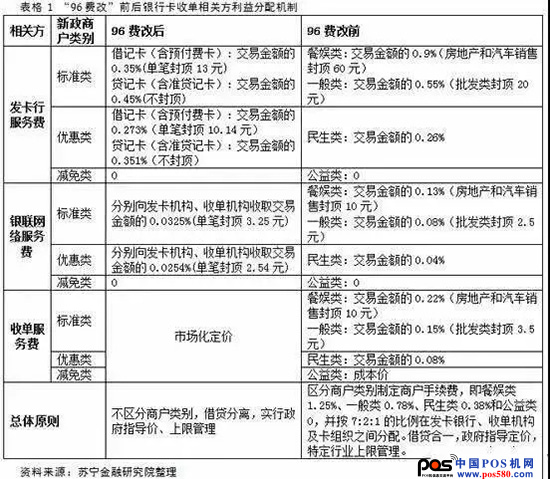

In other words, before the fee is changed, the merchant will pay a handling fee of 0.78%, and the ratio of the three accounts is 7:1:2.

Issuer: 0.55%

UnionPay: 0.08%

Acquirer: 0.15%

However, the fee for the card handling fee was adjusted after September 6, 2016. And the proportion of the entire system has also changed. The original issuer, UnionPay, and acquirer, the ratio of the three parties 7:1:2 has been broken.

After the fee change, this ratio becomes:

Card issuer: 0.45%

UnionPay: 0.065%

Acquirer: 0.085%

Let's continue to analyze the costs and profits of these three institutions.

First, the bank (issuing bank)

This is the largest piece of the "fee" and 0.45% is for the bank. It seems that the bank has the most, but in fact the bank has not made any money.

Because the bank has to provide three major benefits:

1) Points redemption gifts;

2) interest-free period;

3) Various interests, wool

Among them, "point redemption gifts", although the major banks are dazzled, but the overall average is roughly 0.2%, each bank may have nuances. All kinds of rights and interests, wool, banks have their own marketing expenses budget, and will not be put into cost discussion for the time being. In this way, the bank gets 0.45%, and after deducting 0.20% of the gift, there is still 0.25% left. This 0.25% is responsible for your "interest-free period". Under normal circumstances, the average customer account period card is not tight. The average interest-free assumption is 42 days, then the "cost of capital" is about 3% per year. That is, you have swiped the card at the merchant, and the bank lends you 3% of the annual rate of funds, borrowing for a month and a half. So from here you can see that this rate, the bank does not make money.

Second, UnionPay

When I swiped my card in the early 1990s, I wonder if you still have an impression. If you go to the "first department store" to buy things, put a dozen POS machines in front of the checkout counter.

If you are printing a Chinese bank card, the cashier girl will pick up a BOC POS.

If you are printing an ICBC card, the cashier girl will pick up a business POS.

If you are building a bank card, the cashier girl will pick up a CCB POS.

Until "Zhu Rongji", an important purpose in the "Golden Card Project" was "interconnection". Since then, there is only one "UnionPay" POS machine at the checkout counter.

The current process has become: Swipe----- UnionPay----- Bank. Among them, UnionPay charges a fee of 0.065%.

UnionPay charges seem to be the least of the three, but correspondingly, UnionPay pays the least amount of labor and costs. Therefore, UnionPay is the most profitable one. (Relying on the government "monopoly license")

Of course, there are people who don’t believe in evil. The most typical example is "Alipay."

When you first started watching the Alipay Ver 1.0 interface in 2004. He is not the Alipay shield interface of today's "unification." At that time, if you bought clothes for Taobao, Alipay paid. As soon as the page opens, hey, there are dozens of online banking. Really dozens. Almost every big bank with a name. He has it all over.

Ma Yun is based on this idea;

"It's a silly thing to do a dozen POS machines, but it's not easy to give you a dozen buttons on the Web." So when Alipay came out, UnionPay "jumped". No matter which card you have, the 30 banks that Alipay supports, you can brush. Bypassed UnionPay.

Alipay later asked customers for fees, but the price was still cheaper than UnionPay. This is the popular scan code payment.

Third, the acquiring institution

The receipt is a huge manpower industry with hundreds of thousands of employees. When you go shopping, the salesperson takes out a POS machine to let you swipe your card. Have you ever thought about how much this POS machine costs? How did this POS machine go to every store?

To do this, it is called "acquisition." The receipt is a bitter haha ​​young man carrying more than a dozen machines and running to various shops. "Grandpa, Grandma, please beg you to install a machine"; Visit once a month if you print paper When you are done, give you a new paper roll cartridge for free. Looking at the tens of millions of merchants in China, this is done by a "manpower" family. After that, the operation and maintenance is also coming to the door every month.

"Acquiring" is a labor-intensive job. A small shop in the streets and lanes swept over, signed an agreement, and bowed his head. Among the whole commission cakes, the "acceptance" took away a little bit, and the heavens were authentic. Therefore, the receipt of a single is a meager profit, earning some hard money.

From the above analysis, we can see that the "payment" chain, the profit is very meager, you have eaten at the seafood hotel, brushed 1,000 yuan, lobster, geoducks may have hundreds of dollars of gross profit, but " Paying "links, you have only spent 6 yuan to give: the three institutions of the receipt + UnionPay + Bank. Every institution earns a few cents of sand.

Therefore, there is no point in the "no commission" transaction. This is also fair and reasonable

For example: a Platinum card, the amount of 200,000 yuan, one and a half month interest-free period. Even in accordance with the internal accounting of the bank, it costs nearly 750 yuan. You only need to charge 80 yuan for the capping machine, and then according to the ratio of 2/1/7, the bank will get 56 yuan. So the bank is very resentful.

According to the bank's internal "big data" accounting method, if you brush 0.6% of the UnionPay standard machine, the bank can be divided into 0.45%, deducting the integral feedback, and 0.25%, barely supporting the cost. Because the bank will count, when your "loss amount" reaches a certain level. The bank will find an excuse to "close" your card. The excuse is not important, you can't declare it anyway.

There is also a situation, the code hopping machine, the offline jumper: you obviously brushed the 0.6% standard machine. But in the end, I didn't get the points. This may be a "hopping machine" because the competition is fierce now. The profit of the payment company is also very small. Even as low as a loss, they will find a way to eat your money. Obviously you are brushing 0.6% of the machine, but when switching the line, it cuts to a low-rate or even zero-rate machine (such as a public welfare class); thus he swallows up your money. You obviously brushed the restaurant business, and the last ticket shows "XX School" "XX Hospital"

The code hopping code has always existed. Nowadays, many online transactions are used, that is, the online fast payment channel. Some card friends said: Recently, a certain 5,000 yuan or more trading hop discount category, 5,000 yuan or less jump line is fast. Offline rates are higher than online

In fact, many hand brush companies can't compete with similar products in the market if they don't jump. The agent will dislike the product rate is too high to be a market, and can not quickly expand the market, so this has caused a vicious circle of low-rate competition.

Some hand brush companies, long ago, began to layout "hopping fast channel", the system recorded the user's credit card four elements, with four elements, do not swipe, the transaction amount is small (generally in the thousands or so) even Don't use passwords [theoretically, you can deduct money for deductions], but in order to prevent users from worrying about being too unsafe, and to prevent the regulatory authorities from discovering, the technicians must be perfect so that users can't feel the "offline card transaction" change. Became an "online quick deal."

Since the beginning of the 96 fee reform, the clear text stipulates that the credit card rate cannot be lower than 0.6%. However, in order to seize the market, many companies have introduced low rates to enable users to register and use. They do not know the conspiracy behind them, for their own card security, far from low. Rate (wool is on the sheep).

After reading the specific reasons and quantity of the above three agencies, I believe you have understood that the rate is fixed at 0.6%, the cost of UnionPay cannot be reduced, and the fixed cost; if the bank’s expenses are reduced, the card is unfavorable, and the derating is sealed. Card; the cost of hard-earning expenses of the acquiring institution cannot be changed. The above two hard expenditures add up, not the cost of the acquiring institution is about 0.52%. So what is the situation with POS machines that are below the 0.6% rate on the market?

We can often see some 0.58%, 0.55% or even 0.50% machines in the market. It is conceivable that their third-party payment companies, acquirers and agents will not only have no profit at all, but also lose money. Together with the company's operating costs, personnel costs, after-sales service, these are all funds. Businesses are not philanthropists, and it is certainly impossible to make money. Therefore, these low-rate machines will sneak into the public goods and preferential businesses to reduce costs and make profits. They squeezed out the bank's profits. In the final analysis, the bank's income has become less, so the final business is still profitable, and the only users who are hurt are the card users themselves!

Think about it, if you are a bank, you can provide a card for the customer service free of charge, providing various activities, wool and interest-free period. As a result, customers will brush these preferential categories and public welfare merchants to make the bank lose money every day. What do you do?

The acquiring institution, payment company, and agency are not philanthropists, nor are banks. Therefore, derating and sealing are the most direct and effective methods and results. Therefore, the machine brushed below 0.6 is more likely to hurt the card, derating, sealing the card, closing the black house.

In fact, the pos machine is not the rate of who is low, and the low 10,000 yuan can not be a few dollars; it is not cheaper than anyone's machine, and cheaper can not be worth the money security.

Cheap machines and rates, problems are not very troublesome after the sale, especially linked to money, if not less than the account is not a few dollars! Compared with the derating of your credit card, this amount of money is a matter of discretion! As for those who are looking for a "lossless" path, I only say one thing, and the last ones are damaged.

Welcome to talk together, I hope everyone can learn.

1:Material: glossy art paper , cardboard, greyboard

2:Customized size & color

3:MOQ: 500-1000 units

4:High quality and competitive price

|

Item Name |

3D Lenticular Puzzle |

|

Material |

plastic + 850gsm Greyboard |

|

Puzzle Size |

30.4*22.8cm |

|

Puzzle thickness |

1.8mm |

|

Printing & Coating |

4C/0C, glossy Varnishing |

|

Box size |

19.5*27*6.1cm |

|

Box Material |

plastic +250gsm gsm CCNB+ E-Fluting |

|

Printing & Coating |

4C/0C, glossy/matte lamination |

|

Weight per box |

870g |

| Package | 10 units per carton |

| G.W. | 9.6KGS |

3D Puzzle,Heart Puzzles,Custom Jigsaw Puzzle,100 Puzzle For Kids

Hangzhou Wonderlandtoys Co., Ltd , https://www.wonderlandtoyscn.com