A simulation study on the impact of carbon taxation on China's macroeconomic and carbon emission reductions:

Based on dynamic CGE model (GAMS software)

This article was written by Yu Feng, published by China Science Software Network.

I. Introduction

With the rapid consumption of natural resources, the massive discharge of pollutants and the deteriorating ecological environment, the frequent smog weather has made us deeply understand and realize the urgency and inevitability of developing a low-carbon economy. Since 2007, China’s total CO2 emissions have surpassed that of the United States, ranking first in the world. In 2009, the government announced for the first time in a binding manner that by 2020, China’s carbon dioxide emissions per unit of GDP will be 40% lower than in 2005. -45%. However, China's energy status of “rich coal, low gas, and lack of oilâ€, as well as the huge energy demand accompanying industrialization, urbanization and modernization, have made China's future carbon emission situation increasingly severe. With the progress of international climate negotiations and the pressure on domestic emission reductions, the imposition of a carbon tax is imminent, but for various reasons, China has not implemented a carbon tax. From a technical perspective, how is the carbon tax levied? How much is levied? What impact will the carbon tax have on China's social welfare, macroeconomics and related industries? Does the “double dividend†effect of the carbon tax exist? These are all issues that need to be resolved and clarified.

Due to the influence and spread of carbon tax collection, it involves the entire economic system of industry, residents, government, etc. Therefore, from the international literature, most scholars have adopted a strict theoretical system and can simulate and analyze each other within the economic system. The computational general equilibrium (CGE) model of the mechanism of action is simulated. The representative documents are: Whalley and Wigle (1990), Burniaux and Nicoletti (1992), Floros and Vlachou (2005), Galinato and Yoder (2009). Allan G. et al. (2014), in general, foreign studies on the application of CGE models for carbon tax research are relatively mature. In recent years, domestic research on carbon taxes has also increased. He Juhuang, Shen Keting et al. (2002) established a static CGE model to analyze the impact of carbon tax on various sectors of the national economy; Zhu Yongbin et al. (2010) based on a static CGE model, by introducing a carbon tax, assuming six scenarios for carbon tax policy The effect of emission reduction and its impact on macroeconomics and various industrial sectors; Guo Zhengquan et al. (2012) analyzed the impact of carbon taxation policies on energy demand and carbon dioxide emissions in China's development of low carbon economy based on static CGE model; Shi Minjun et al. (2013) Using the CGE model, a single carbon tax, a single carbon emissions transaction, and a composite policy of carbon tax and carbon trading were designed to simulate the emission reduction effects, economic impacts and abatement costs of different policies. Different from the above domestic literature, Wang Can (2005) constructed a dynamic CGE model based on the 1997 input-output table, and used this model to simulate and analyze the hypothesis that the total CO2 emissions in the baseline scenario is reduced by 10%-60%. Marginal abatement costs, economic growth and the impact of employment.

From the literature point of view, most of the domestic carbon tax CGE models are static models. There are few domestic literatures on the application of dynamic CGE models to analyze carbon taxes. Since the static CGE model can only be simulated within the base year, it cannot dynamically simulate carbon tax. The long-term cumulative effect, so the simulation analysis function of the static CGE model is more limited. Although Wang Can (2005) constructed a dynamic CGE model, the simulation hypothesis of this paper lacks practical significance, because China's total carbon dioxide emissions are increasing every year, and the total amount of carbon dioxide is reduced before China's urbanization and industrialization stages are not completed. The assumptions are difficult to establish; the carbon dioxide emission reduction targets in the national “Twelfth Five-Year Plan†are also set to reduce carbon dioxide emissions per unit of GDP, which is a relative indicator and not a reduction in the total amount of carbon dioxide.

Based on the previous studies and the characteristics of China's economy, the computable general equilibrium model constructed in this paper has the following characteristics: 1 From the technical level, this paper constructs a recursive dynamic CGE model for carbon based on the latest dynamic economic theory. Tax policy simulation; 2 according to the national environmental protection “Twelfth Five-Year Planâ€, adopting relative indicators, that is, measuring carbon dioxide emissions per unit of GDP as a target; 3 further dividing energy into clean energy and petrochemical energy (Petrochemical energy is further subdivided into coal , oil and gas), using a multi-layer CES function nesting method to combine, and comprehensively simulate the carbon tax and related carbon dioxide emission reduction from the carbon tax collection method and the carbon tax use method.

Second, the dynamic computable general equilibrium (DCGE) model construction

1. Macro micro SAM table construction and data source

This paper is based on the input and output table of China's 2007 135 sector [1]. The merger is expanded into one primary industry sector, 15 secondary industry sectors and five tertiary industry sectors. The actors are divided into government and households. , enterprise, investment and savings, foreign sector's macro social accounting matrix (SAM) table, the data in this table is not only from the 2007 input-output table, but also from China Statistical Yearbook 2008, China Financial Yearbook 2008 , "China Environmental Yearbook 2008", "balance of payments 2008", "China Energy Statistics Yearbook 2008" and other statistical data. Building a micro-SAM on a macro-SAM basis, one important detail is the splitting of the power sector and the petrochemical energy sector (even the 135 sector input-output table, oil and gas as a sector; electricity as a sector, no fine Splitting thermal power, hydropower, wind power, etc., the method of splitting is as follows: According to the proportion of power production in the 2008 China Electricity Statistical Yearbook, the power sector in the input-output table accounts for 83.06% of thermal power, nuclear power and other power supplies. The proportion of 16.94% is split. Among them, coal, oil and natural gas only have intermediate inputs for the production of thermal power. There is no intermediate input decomposition for nuclear power and other power supply. The decomposition of oil and natural gas exploitation is based on China's energy production in 2007. Among them, oil accounts for 19.70% of total energy consumption; natural gas accounts for 3.50% of total energy consumption, and then splits the input-output table data according to the proportion of consumption.

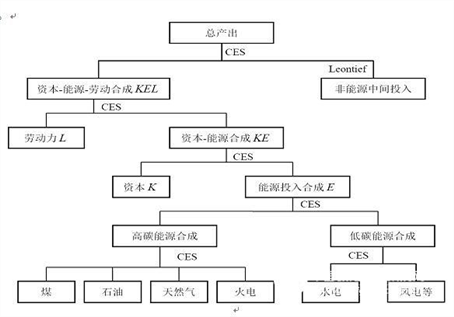

2. Production function structure design

The production structure of the dynamic CGE model in this paper adopts a five-layer nested structure, which is one of the mainstream methods in the international academic community. The combination of intermediate inputs only contains non-energy inputs (the Leontief function expresses its relationship), but Energy, capital, and labor are nested using the Constant Elasticity of Substitution (CES). The nesting structure of capital-energy-labor CES synthesis is combined from bottom to top according to the degree of substitution of various energy inputs, as shown in Fig. 1.

Figure 1: Schematic diagram of the production function structure

Third, carbon tax design and simulation analysis

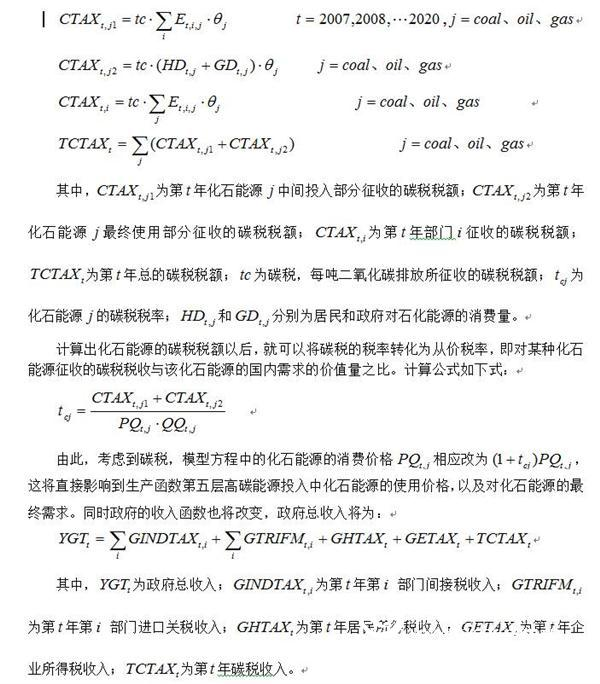

1. Carbon tax designIn this paper, the CGE model is used for policy simulation. The taxation basis is CO2 emission, and the internationally used taxation method for fossil energy use is adopted. The specific carbon tax design is as shown in the following equation:

2. Policy Simulation 1: Simulation Analysis of Carbon Tax Collection Method

First, the effects of different carbon tax levels on China's carbon dioxide emission intensity and its marginal rate of change, as well as sectoral output and price variables, are simulated during 2007-2020. Due to the carbon tax collection, the increase in petrochemical energy use costs will inevitably lead enterprises to actively improve energy efficiency through research and development or other means. Therefore, this paper imposes a carbon tax and assumes that energy use efficiency also changes, thus comprehensively simulating carbon tax. The effect of emission reduction.

Table 4 Carbon Tax Collection Scheme Simulation Scenario Table

Scenario category

specific description

Baseline scenario

The total labor supply is exogenous in 2007-2020. As shown in Table 3, energy efficiency remains unchanged and carbon tax is not considered.

Scenario I

Based on the baseline scenario, the annual growth rate of energy use efficiency is 0%, and a carbon tax is imposed.

Simulation scenario II

Based on the baseline scenario, the energy use efficiency is growing at an annual rate of 0.5% and a carbon tax is imposed.

Simulation scenario III

Based on the baseline scenario, energy use efficiency is growing at an annual rate of 1%, with a carbon tax.

Simulation scenario IV

Based on the baseline scenario, the energy use efficiency is growing at an annual rate of 2% and a carbon tax is imposed.

(1) Analysis of energy and carbon emissions impacts

Table 5 China's carbon dioxide emission intensity and its marginal rate of change under different carbon tax levels at the end of 2020

Carbon tax (yuan/ton)

Scenario I

Scenario II

Scenario III

Scenario IV

Carbon dioxide emission intensity (%)

Marginal rate of change in carbon dioxide emission intensity per unit carbon tax (%/unit carbon tax)

Carbon dioxide emission intensity (%)

Marginal rate of change in carbon dioxide emission intensity per unit carbon tax (%/unit carbon tax)

Carbon dioxide emission intensity (%)

Marginal rate of change in carbon dioxide emission intensity per unit carbon tax (%/unit carbon tax)

Carbon dioxide emission intensity (%)

Marginal rate of change in carbon dioxide emission intensity per unit carbon tax (%/unit carbon tax)

0

0.000

-4.588

-8.701

-15.561

5

-4.957

0.000

-9.391

-0.480

-13.375

-0.467

-20.024

-0.446

10

-9.286

-0.496

-13.581

-0.419

-17.435

-0.406

-23.883

-0.386

15

-13.102

-0.433

-17.263

-0.368

-20.997

-0.356

-27.258

-0.337

20

-16.500

-0.382

-20.537

-0.327

-24.156

-0.316

-30.240

-0.298

25

-19.540

-0.340

-23.461

-0.292

-26.980

-0.282

-32.891

-0.265

30

-22.287

-0.304

-26.098

-0.264

-29.521

-0.254

-35.273

-0.238

35

-24.775

-0.275

-28.485

-0.239

-31.817

-0.230

-37.426

-0.215

40

-27.047

-0.249

-30.662

-0.218

-33.912

-0.209

-39.382

-0.196

45

-29.128

-0.227

-32.656

-0.199

-35.825

-0.191

-41.165

-0.178

50

-31.045

-0.208

-34.487

-0.183

-37.579

-0.175

-42.800

-0.163

55

-32.814

-0.192

-36.179

-0.169

-39.204

-0.163

-44.310

-0.151

60

-34.453

-0.177

-37.747

-0.157

-40.705

-0.150

-45.705

-0.140

65

-35.983

-0.164

-39.204

-0.146

-42.105

-0.140

-47.004

-0.130

70

-37.407

-0.153

-40.566

-0.136

-43.404

-0.130

-48.207

-0.120

75

-38.739

-0.142

-41.836

-0.127

-44.621

-0.122

-49.334

-0.113

80

-39.990

-0.133

-43.030

-0.119

-45.762

-0.114

-50.393

-0.106

85

-41.170

-0.125

-44.151

-0.112

-46.836

-0.107

-51.385

-0.099

90

-42.277

-0.118

-45.211

-0.106

-47.848

-0.101

-52.320

-0.093

95

-43.327

-0.111

-46.208

-0.100

-48.802

-0.095

-53.202

-0.088

100

-44.319

-0.105

-47.152

-0.094

-49.703

-0.090

-54.036

-0.083

It can be seen from Table 5: (1) When the carbon tax is not considered, when the energy use efficiency is increased by 0%, 0.5%, 1%, and 2%, respectively, the carbon dioxide emission intensity in China can be reduced by 0% and 4.59 respectively compared with the baseline scenario in 2020. %, 8.70% and 15.56%; when considering the carbon tax, when the energy use efficiency is increased by 0%, 0.5%, 1%, 2%, respectively, the carbon dioxide emission intensity in China can be reduced by 44.32% and 47.15% in 2020, respectively. 49.70% and 54.04%; (2) To achieve the goal of “China’s carbon dioxide emissions per unit of GDP will be 40%-45% lower by 2020 than in 2020†in the “Twelfth Five-Year Planâ€, only consider improving energy efficiency and carbon Under the premise of taxation, if the annual growth rate of energy use efficiency is 0%, the carbon tax will be about 80 yuan/ton; if the energy use efficiency is 0.5%, the carbon tax will be about 70. RMB/ton; if the annual growth rate of energy use efficiency is 1%, the carbon tax will be about 60 yuan/ton; if the energy use efficiency is 2%, the carbon tax will be about 40 yuan/ton; (3) Strong carbon dioxide emissions per unit carbon tax under the four scenarios Marginal change ratios exhibit decreasing trend, comparatively speaking, the higher the energy efficiency, the greater the rate of change in CO2 intensity marginal unit of carbon tax.

Table 6 Advance tax rate of fossil energy under different carbon tax levels during 2007-2020

years

In scenario I, the annual growth rate of energy use efficiency is 0%, and the carbon tax is 80 yuan/ton.

In scenario IV, the annual growth rate of energy use efficiency is 2%, and the carbon tax is 40 yuan/ton.

Change rate of carbon dioxide emissions per unit of GDP relative to the baseline scenario (%)

Coal tax rate (%)

Oil tax rate (%)

Natural gas tax rate (%)

Change rate of carbon dioxide emissions per unit of GDP relative to the baseline scenario (%)

Coal tax rate (%)

Oil tax rate (%)

Natural gas tax rate (%)

2007

-0.76

74.05

5.61

7.73

-0.51

31.24

2.35

3.18

2008

-0.78

76.91

5.87

8.12

-0.54

32.83

2.50

3.36

2009

-0.80

79.54

6.11

8.48

-0.58

34.30

2.66

3.53

2010

-0.82

81.92

6.34

8.81

-0.62

35.68

2.81

3.70

2011

-0.83

84.12

6.56

9.13

-0.64

37.00

2.96

3.85

2012

-0.85

86.15

6.78

9.43

-0.68

38.26

3.11

4.00

2013

-0.86

88.04

6.99

9.71

-0.70

39.46

3.27

4.15

2014

-0.87

89.83

7.20

9.97

-0.73

40.62

3.42

4.29

2015

-0.88

91.54

7.41

10.23

-0.75

41.74

3.58

4.43

2016

-0.89

93.19

7.61

10.48

-0.78

42.84

3.73

4.56

2017

-0.90

94.81

7.82

10.72

-0.81

43.93

3.90

4.69

2018

-0.91

96.82

8.15

11.03

-0.84

45.14

4.10

4.84

2019

-0.91

98.04

8.26

11.21

-0.86

46.13

4.23

4.96

2020

-0.92

99.70

8.48

11.46

-0.89

47.27

4.41

5.09

Table 6 shows that, under other conditions, the carbon tax alone can achieve the national “12th Five-Year Plan†target for carbon dioxide emission intensity, but this will cause a sharp rise in fossil energy prices. As shown in Table 2: When the carbon tax rate is 80 yuan / ton, in 2007, coal prices increased by 74.05%, oil and natural gas prices will increase by 5.61% and 7.73%, respectively; in 2020, coal, oil and natural gas prices respectively 99.70%, 8.48% and 11.46%, which will inevitably lead to greater price pressures; however, if carbon tax reduction policies are implemented, technological progress will be enhanced and energy efficiency will be improved (such as scenario IV). The tax is about 40 yuan / ton, which can achieve the relevant carbon dioxide emission targets in China's "Twelfth Five-Year Plan". Under this circumstance, the corresponding fossil energy prices in 2007 increased by 31.24%, 2.35% and 3.18% respectively. The price of fossil energy increased by 47.27%, 4.41% and 5.09% respectively, and the pressure on price increases decreased significantly. If energy efficiency is further improved, the corresponding carbon tax will continue to decrease, and the space for fossil energy price increases will further narrow.

(2) Departmental impact analysis

The carbon tax will inevitably lead to an increase in fossil energy prices, which will increase production costs. The proportion of fossil energy inputs in different sectors will vary greatly, and the substitutional elasticity of production functions and various production factors at different levels will not be exactly the same. And the difference in demand for products from different sectors will have an inconsistent impact on fossil energy demand in different sectors. Thus, the output price, output, labor, capital use, carbon dioxide emissions, carbon dioxide emission intensity of the sector Etc. will have different effects. Table 7 shows that in scenario I, the annual growth rate of energy use efficiency is zero (the energy use efficiency remains unchanged from the baseline scenario), and the output of each sector in 2010, 2015 and 2020 when the carbon tax is 30 yuan/ton. And its price is affected by changes in the baseline scenario.

Table 7 Sectoral output and price impact relative to the baseline scenario

industry

year 2010

2015

2020

output(%)

price(%)

output(%)

price(%)

output(%)

price(%)

agriculture

-2.6091

1.0311

-2.1252

0.9587

-2.0255

0.9140

Coal mining and coking industry

-46.8959

9.4921

-49.9630

10.2474

-51.9491

10.8880

Oil extraction and processing industry

-12.8238

9.9966

-14.6663

10.9261

-15.7323

11.6744

Natural gas mining industry

-9.8966

4.8505

-11.5029

5.1692

-12.5058

5.4663

Food manufacturing and tobacco processing industry

-2.4061

1.4400

-2.1449

1.3496

-2.0733

1.3081

Textile industry

-12.8411

3.1151

-6.5711

2.5232

-4.4799

2.2771

Wood processing and furniture manufacturing

-0.1412

3.0661

-1.8961

2.8172

-2.2335

2.6779

Paper printing press, stationery, manufacturing

-5.7136

3.1691

-3.9407

2.9423

-3.0653

2.8171

Chemical and pharmaceutical industry

-9.9556

5.4804

-8.0918

5.5951

-7.1725

5.6948

Non-metallic mining and non-metallic mineral products industry

5.6461

7.1517

-0.3464

7.5251

-2.2694

7.8426

Metal mining and metal smelting industry

-4.4349

5.4498

-6.5836

5.5490

-6.7875

5.6019

Mechanical equipment manufacturing

0.9902

3.4386

-2.4551

3.2300

-3.2178

3.0500

Electronic communication, instrument office manufacturing

-27.1501

2.5954

-11.7434

1.9399

-6.9555

1.6790

Other manufacturing

-3.1379

1.8784

-4.1250

1.7423

-4.1351

1.6962

Electricity (thermal power) production and supply industry

-3.2686

13.3257

-3.8722

14.4043

-3.9662

15.3438

Low-carbon energy (hydropower, wind power and nuclear power) production

0.1187

1.8877

0.2645

2.2102

0.4378

2.5479

Construction industry

15.5257

4.0906

4.1320

4.0723

0.5126

4.0366

Transportation, warehousing and postal services

-1.1239

2.6693

-2.6204

2.7648

-3.0300

2.8803

Wholesale, retail and accommodation industry

-0.9247

0.8827

-1.4016

0.7908

-1.6400

0.7592

Finance and real estate

-0.1475

0.4505

-0.5604

0.2980

-0.8140

0.2587

Science, education, culture, social service

3.5407

1.7941

3.7424

1.6787

3.8939

1.6156

The results in Table 7 show that in 21 industries, output prices have risen, mainly due to the carbon tax, which has led to an increase in production costs. Among them, coal, oil, natural gas industry and fossil energy consumption are large. The prices of electricity (thermal power), non-metallic mineral mining and non-metallic mineral products, metal mining and metal smelting industries have increased by a large margin, and in terms of time, their price increases have increased year by year; Prices in the lower energy sectors of agriculture, finance and real estate, wholesale and retail and lodging, food manufacturing and tobacco processing, science, education, culture and social services have risen significantly, and, in terms of time, their prices have risen. The magnitude is decreasing year by year.

In terms of output, among the 21 industries, coal mining and coking, oil extraction and processing, and natural gas mining have the largest declines in output, and their output declines further as time goes by; although textile The output of industry, chemical and pharmaceutical industry, electronic communication, and instrumental office manufacturing has a large decline in output at the beginning of the period [2], but unlike the fossil energy sector, its decline has gradually decreased over time; It is worth noting that the output of low-carbon energy (hydropower, wind power and nuclear power) industries is increasing year by year, mainly because the replacement of low-carbon energy has gradually emerged after the price of fossil energy has increased, and social demand has increased, and With the extension of time, its substitution effect is gradually strengthened.

3. Policy Simulation 2: Simulation Analysis of Carbon Tax Usage

Generally speaking, carbon tax will cause the price of fossil energy to rise, which will lead to higher production costs and higher product prices. However, different dynamic recycling methods of carbon tax may lead to different corporate income, household income, household consumption, and government savings. Social and economic variables such as imports and exports and social welfare have changed. In addition, there is still an effect in the academic world on whether the carbon tax can achieve the “double dividendâ€. Therefore, this paper takes the carbon dioxide emission intensity reduction by 20% in 2020 as an example, and simulates the different carbon tax recycling methods for the social economy. The impact of variables. The specific scenarios are set as follows:

Table 8 Carbon Tax Usage Simulation Scenario Table

Scenario category

specific description

Baseline scenario

The total labor supply is exogenous in 2007-2020. As shown in Table 3, energy efficiency remains unchanged and carbon tax is not considered.

Scene V

On the basis of the baseline scenario, a carbon tax is imposed on energy consumption, and various tax rates remain unchanged.

Simulation scenario VI

On the basis of the baseline scenario, carbon tax is imposed in the energy consumption sector, while reducing the income tax rate of residents and keeping the government's fiscal revenue neutral. At this time, the resident income tax rate becomes an endogenous variable, and the government fiscal revenue is exogenous in each year, which is equivalent to the government fiscal revenue in each year in the baseline scenario.

Simulation scenario VII

On the basis of the baseline scenario, carbon tax is imposed in the energy consumption sector, while the corporate income tax rate is lowered, and the government's fiscal revenue is neutral. At this time, the corporate income tax rate becomes an endogenous variable, and the government fiscal revenue is exogenous in each year, which is equivalent to the government fiscal revenue in each year in the baseline scenario.

Simulation scenario VIII

On the basis of the baseline scenario, the carbon tax is imposed in the energy consumption sector, and the indirect tax rate is reduced. Because the indirect tax rate of the department is not the same, an average indirect tax rate variable is added, which is endogenous, so that the indirect tax rate of the department changes the same. Percentage; maintaining the government's fiscal revenue neutral, at this time, the average indirect tax rate is an endogenous variable, and the government fiscal revenue is exogenous in each year, which is equivalent to the government fiscal revenue in each year in the baseline scenario.

Table 9 2020 macroeconomic and social variables under different scenarios[3]

Scene V

Scenario VI

Scenario VII

Scenario VIII

Real GDP (%)

-0.9381

-1.0125

-0.6769

-0.5832

Social welfare [4] (%)

-2.5150

4.7609

-2.8360

-0.5642

residence income(%)

-0.2115

-0.4827

-0.2744

-0.2377

Household consumption (%)

-0.7951

1.5051

-0.8966

-0.1784

Household savings (%)

-0.1202

-0.5749

-0.1395

-0.2563

Business income (%)

-0.9983

-1.3356

-0.4747

-0.4499

Corporate savings (%)

-0.9983

-1.3356

7.1280

-0.4499

Government savings (%)

4.9710

0.0000

0.0000

0.0000

Government consumption (%)

4.3652

-0.4545

-0.8067

-0.1235

Export(%)

-6.3556

-5.8329

-6.8351

-1.7216

import(%)

1.4447

0.9634

2.8395

0.3572

Total investment

-0.4143

-2.2675

2.9051

-1.1275

Carbon dioxide emission intensity

-19.9856

-20.0336

-19.9856

-20.0384

The changes in the macroeconomic variables in scenarios V, VI, VII, and VIII were compared and analyzed based on the analysis results in Table 9. In scenario VI, compared with the baseline scenario, due to the carbon tax, the capital income of residents has decreased. Although the government has reduced the personal income tax of residents while collecting carbon tax, the government’s transfer payment to residents has also declined. The personal income tax amount is lower than the government transfer payment, so the total pre-tax income level of the residents is larger than that of the scenario V. However, due to the reduction of the personal income tax rate, the residents' after-tax income has increased, and the residents' consumption demand has increased. Improvement, so the social welfare status of residents is significantly improved compared to scenario V. Under the circumstance that the total tax relative to the baseline scenario remains unchanged, the government's physical consumption is reduced due to the increase in product prices due to the carbon tax levy. For enterprises, the carbon tax has led to an increase in production costs, which has led to a relative decline in capital prices. As a result, corporate income and consumption levels have been greatly reduced. At the same time, as domestic product prices have risen relative to foreign countries, exports have decreased significantly, and imports have increased. . Among the actual GDP composition, only the relative consumption of residents has increased, while government consumption, investment, and import and export have all decreased, resulting in a decline in real GDP. Overall, Scenario VI has increased the level of social welfare while reducing the intensity of CO2 emissions, thus achieving the “double dividend†effect of carbon tax.

In Scenario VII, compared with the baseline scenario, for the enterprise, the capital price is reduced due to the carbon tax, and the income of the enterprise is reduced. However, due to the reduction of the corporate income tax rate, the level of corporate savings has been greatly improved. Residents due to the decline in capital income, government transfer payments, the overall income of residents decreased, resulting in a greater decline in household consumption, household savings, and social welfare levels compared to scenario V. Although the government’s income and savings have not changed, the government’s physical consumption has fallen the most because of the large increase in product prices. The reason for the decline in real GDP is the same as above, but the real GDP decline is smaller than scenario V and scenario VI. Overall, scenario VII low corporate income tax has led to an increase in corporate savings and total investment, but also resulted in a larger decline in household consumption and social welfare levels compared to scenario V and scenario VI. This shows that the reduction of corporate income tax while reducing the carbon tax can not achieve the "double dividend" effect of carbon tax.

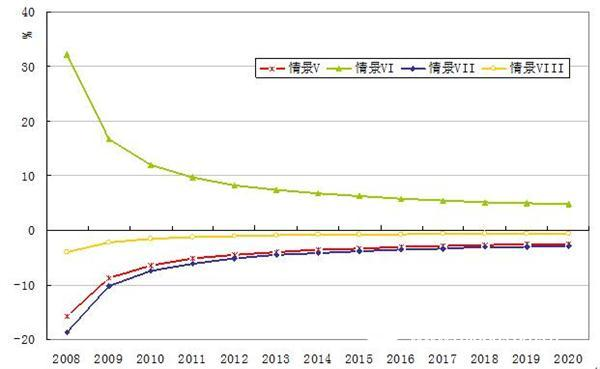

Figure 2 Social welfare changes in different scenarios during 2008-2020

In scenario VIII, because indirect taxes are reduced and indirect taxes occur in domestic production, companies can partially pass the tax burden on consumers, thereby affecting domestic demand and exports. Therefore, although the income of enterprises in this scenario has declined, But the decline is smaller than the other three scenarios. For the residents, the labor income and capital income of the residents have decreased, and the government transfer payment has also decreased. Therefore, the total income level of the residents has slightly decreased compared with the scenario V. However, the price of domestic products has decreased due to the reduction of indirect taxes. Residents' consumption needs and social welfare levels have improved compared with Scenario V and Scenario VII. The government's income and savings remain unchanged, but as domestic product prices have declined, the government's physical consumption has increased compared to scenario VI and scenario VII. As the consumption of residents, government consumption, and net exports improved significantly, the decline in real GDP was the smallest compared to the other three scenarios. As can be seen from Figure 2, in scenario VIII, social welfare declines are small and close to zero over time. This shows that the reduction of corporate indirect taxes while imposing a carbon tax can make the impact of carbon tax on social welfare very small.

Conclusions and recommendations

1. Under other conditions, the carbon tax alone can achieve the national 12th Five-Year Plan for carbon dioxide emission intensity, but this will cause a sharp rise in fossil energy prices, which will cause greater price pressures; However, in the process of strengthening scientific and technological progress and implementing energy tax reduction policies under the premise of improving energy efficiency (2% annual growth rate), the 40 yuan/ton carbon tax collection standard can realize China’s “Twelfth Five-Year Planâ€. The target for carbon dioxide emissions. In addition, with the increase of the carbon tax rate, the marginal rate of change of carbon dioxide emission intensity per unit carbon tax has gradually decreased. In comparison, the higher the energy use efficiency, the marginal rate of change of carbon dioxide emission intensity per unit carbon tax. The bigger. Therefore, improving energy efficiency can effectively enhance the implementation of carbon tax. China should strengthen technological innovation and management innovation, and promote the continuous improvement of energy efficiency in China.

2. In terms of industry, output prices have risen in 21 industries, including coal, oil and natural gas industries and electricity that consumes more fossil energy (thermal power), non-metallic minerals, and non-metallic mineral products. The prices of metal mining and metal smelting industries have increased by a large margin, and in terms of time, their price increases have increased year by year. Prices in the agricultural, financial and real estate industries, wholesale and retail and accommodation industries, food manufacturing and tobacco processing industries, science, education, culture and social services industries that consume less fossil energy are significantly less, and their price increases are increasing year by year. cut back. In addition, with the increase in fossil energy prices, the output of low-carbon energy (hydropower, wind power and nuclear power) industries is increasing year by year, and the substitution effect is gradually strengthened.

3. If a carbon tax is imposed in the energy consumption sector, and the income tax rate is lowered, and the government's fiscal revenue is neutral, the tax plan can reduce the carbon dioxide emission intensity and increase the social welfare level, thus achieving the carbon tax. The double dividend effect; while maintaining the government's fiscal tax neutrality, the appropriate reduction of corporate income tax while imposing a carbon tax does not achieve the “double dividend†effect of the carbon tax. Therefore, from the perspective of the welfare level of social residents, to achieve the "double dividend" effect of carbon tax, China's carbon tax collection should be synchronized with the resident income tax reform.

4. If a carbon tax is imposed in the energy consumption sector, and the indirect tax rate is lowered, and the government's fiscal revenue is neutral, the tax plan is adopted. In addition, the carbon tax is imposed in the energy consumption sector, and the corporate income tax rate is lowered to maintain the government's fiscal revenue. The plan can weaken or eliminate the negative impact of the carbon tax on the level of social welfare. Therefore, from the perspective of the negative impact of the carbon tax on the level of social welfare, China's implementation of the carbon tax, while reducing the effect of corporate indirect tax on social welfare level is better than the appropriate reduction of corporate income tax.

For more information on GAMS software or dynamic CGE models, please visit the China Science Software Network.

[1] At present, the National Bureau of Statistics has not officially announced the 2010 China Input-Output Table, so the 2007 Input-Output Table can only be used as the data base.

[2] The reason is that the fossil energy elasticity coefficient of the textile industry, chemical and pharmaceutical industry, electronic communication, and instrument office manufacturing industry is relatively high.

[3] Real GDP, household consumption, government consumption, exports, and imports are all quantitative variables; nominal GDP, social welfare, household income, household savings, corporate income, corporate savings, government savings, and total investment are all values. Value variable.

[4] The social welfare of this paper is measured by the Hichsian equivalent variation, which is more commonly used in the international literature. The Hicks equivalent change is based on the commodity price before the policy implementation, and the resident policy is measured. Changes in the level of utility after implementation.

- The living room Sectional Sofa set is features a solid wood and finished with luxurious top grain leather upholstery throughout.Built-in high density sponge,sitting for a long time is not tired, does not collapse, slow rebound.

- Small space configurable sectional;Fashion L-Shaped sectional design to allow for spacious seating.

- Corner Sofa features:Generous armrest can be used as a headrest;Thick cushion, soft and comfortable, relieve fatigue;Full and mellow reclining comfort padded backrest and headrest;The metal feet are firm and stable, providing a strong support for the sofa

- The contemporary sectional couch with an extra wide chaise lounge for maximum comfort,a great choice for home furniture. Ultra soft and durable chaise lounge sofa improve home decoration and quality of life.

- 2 seat sofa with chaise longue,sitting and lying down are natural and relaxing; The shipment will be delivered downstairs only,without installation service

L Shape Sofa,L Shaping Sofa,Living Room Sofas,Living Room L Shape Sofa

Kaifeng Lanwei Smart Home Co., Ltd , https://www.manualrecliner.com