Author: Xue Hong Yan Su Ning, director of Center for Financial Research Institute of Finance, Internet

The new year has begun, and it is time to resign and welcome the new. From the perspective of an industry development, the future is bred in the past, and there is no way to talk about the so-called old and new. As far as the payment industry is concerned, 2016 has a different meaning, making 2017 also confusing, both potential black swan and true and false.

If you want to use a word to summarize the 2016 payment industry, the author is willing to use the word "stunning"; if you want to use a word to look at 2017, the author is willing to use the word "unknown." If you are interested in the payment industry or a practitioner, you may wish to read this article.

Three words and two words to outline payment 2016

For the payment industry, 2016 has a different meaning. From the perspective of the industry, a lot of things happened this year, such as the establishment of three types of accounts, the introduction of the network framework, the compliance of scan code payment, the change of the bill of lading business, and the short-term rise and fall of mobile phone Pay. Many phenomena, such as huge fines, renewal extensions, license mergers and acquisitions, giant cash withdrawal fees, traditional financial layouts, emerging payments, etc., all have a major impact on the industry. One year is enough for the industry to digest, let alone one year. Intensive introduction within. Here, the author does not want to record the account of the flow, and does not want to repeat the interpretation of the key events. It may be necessary to intercept several perspectives and simply outline the changes in the payment industry in 2016.

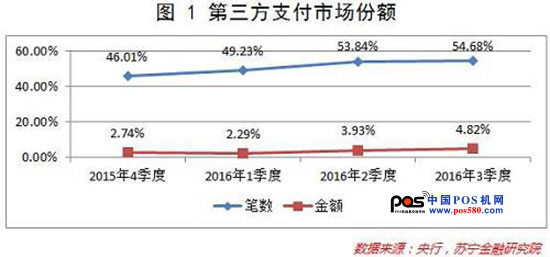

Market share: third-party payment "offensive" fierce

Market share is talkative. According to central bank data, in the first three quarters of 2016, third-party payment institutions handled a total of 111.142 billion online payment services, with a total amount of 68.27 trillion yuan. In the same period, banking financial institutions had a total of 99.132 billion electronic payment services, with a total amount of 18,846,100. 100 million yuan. In terms of the number of pens, third-party payment has been achieved, and the gap in the amount is large, but it has been shrinking.

From the market share [third-party payment network payment business volume 第三方 (third-party payment network payment business volume + bank electronic payment business volume)], in the second quarter of 2016, third-party payment has achieved counter-attack on the number of online payment The amount of money has bottomed out and has continued its upward trend in the third quarter. It can be seen that from the perspective of market share changes, third-party payment is still in the “offensive†in 2016, and the vitality of high-speed development is still there. Difficulties and problems, but the growth is still the same, which probably counts as the most gratifying place for third-party payment in 2016.

Competitive environment: UnionPay counterattack and bank awakening

In the era of big data finance, although the purpose of payment has not changed substantially, the value of payment has far exceeded the payment itself. Payment is no longer just a tool for the transfer of currency claims by both parties to complete the transaction. The customer information, transaction information and other data held by the payment activities are developed and utilized by big data finance, becoming intelligent marketing and big data risk control. Important support. For Internet finance, the existence of third-party payment makes it possible to establish an account system independent of the bank, which greatly accelerates the process of “disintermediationâ€, and the relationship with the bank is dependent on independence or even competition.

Payment has always been the main business of UnionPay. In 2016, UnionPay has launched a counterattack against third-party payment through cloud flash payment (issuing flash payment card, flash payment POS, mobile phone payment, etc.), and the war has just been opened. At the same time, recognizing the change in the value of payment itself, banks no longer regard payment as a common business to create income from intermediary business, but begin to regard it as the cornerstone of internal information integration, customer integration and various banking operations. Awaken and respond. In this regard, you may wish to feel the following signs.

As the most important service window, mobile banking of major banks is now more and more mutually exclusive, and payment transfer has begun to be placed in a prime position. In the past few days, the Bank of China (601988, stocks) APP revised, its display style and Suning financial APP are exactly the same, behind the style change is the transformation of ideas. In addition, the loosening of the scan code and the new rules for the bank's three types of accounts have also cleared the way for banks to make efforts in the payment business.

The giants are awakened, and the competition in the market will be more intense in 2017. The third-party payment practitioners must play a 12-point spirit. For the consumer, the good news is coming. No surprises, the dividend period for paying the subsidy is coming soon.

Policy environment: Pratt & Whitney positioning and arbitrage space disappear

In 2016, as the first year of Internet finance supervision, the policy environment is indeed the biggest variable. The payment industry is also the same, but the author has already had a lot of interpretations, so I won't go into details here. For third-party payments, the biggest impact is the establishment of inclusive financial positioning and the disappearance of policy arbitrage space. The former is reflected in the account limit control and can not open a payment account for financial institutions, while the latter shows that the central bank begins to treat banks and third-party payments equally in the areas of transfer clearing, anti-money laundering, and real-name account.

In the new policy environment, the simple third-party payment license itself has been difficult to bring additional bonuses to the industry. In the face of the awakening of the giants, third-party payment needs to find new outlets and power points.

Two black swans in 2017

Luo Zhenyu mentioned five black swan in 2017 in his New Year's speech. Although some netizens pointed out that this "black swan" is not a "black swan" (can not be called a black swan), the author may also follow the teacher Luo. The definition of the black swan, to talk about the two black swan that the third party will encounter in 2017.

Network connection online, affecting geometry?

For the third-party payment industry that is already used to the bank direct connection model, the online platform of the network connection platform is definitely a big event that can change the industry structure. The key point is that the operating rules after the online line are not fixed, such as whether the bank direct connection mode has a transition. period? How long is the transition period? How to charge for network transfer settlement? In addition to providing clearing services for bank accounts and third-party payment accounts, can the network provide clearing services between third-party payment accounts? and many more. These rules themselves are the key factors that determine the impact of the online connection on the industry. It is precisely because these rules are not determined that the author regards it as the first black swan in the third-party payment industry in 2017.

Who is the beneficiary when the liquidation license is released?

Since 2015, the liquidation of the clearing license has been put on the agenda. In the past few days, the 14th Central Bank and other 14 departments issued the "Opinions on Promoting the Healthy Development of the Bank Card Clearing Market" (Yinfa [2016] No. 324), which clarified the mission of the bank card clearing market and some basic rules, which may mean bank card clearing. The application for the release of the license is approaching.

After the liquidation of the clearing license, there will be one or several clearing institutions that compete directly with UnionPay in the market. For the entire payment industry, the choice to start diversification is whether the election of the sideline team or the long bet will affect the evolution of the market structure. Without any surprise, the network will have a great chance of obtaining a clearing license. In addition to the network, is there a chance for state-owned banks and third-party payment giants? If there is an opportunity, the giant's battlefield will focus on the application for clearing licenses. Will the network association itself become a refuge for small and medium-sized payment institutions to warm up and gradually become marginalized? Based on this, the author regards the release of the clearing license as the second black swan in the industry.

The true and false outlets of third-party payment

The existence of the black swan makes the development of the industry full of variables and difficult to see, but it does not prevent us from looking at the prospect of the industry itself from a higher perspective, the so-called vent. The reason why everyone cares about the slogan is to know where the opportunity is. Where is the trap? The former is the tuyere, while the latter is the pseudo-vent.

Aggregate payment may die from clearing license plate

Recently, the aggregation payment has been inexplicably fired. Some people regard it as a disruptor in the payment industry. I don't agree with this. Aggregate payment is only a phased transition product, and nothing more.

The thing that aggregate payment does is to open up the payment channel of mainstream third-party payment institutions, and realize the function of one-point access and multi-tool connection on the merchant side, which is indeed very convenient. But the problem is that the thing that the aggregation payment tool does is actually the basic function of the network connection platform after obtaining the clearing license. Therefore, before the network connection goes online, there is room for the development of the aggregation payment. After the network connection is online, the aggregation payment is faced first. The problem is that there is no clearing license but doing similar things; moreover, with the network connection, the merchant can directly access the networked POS to support all third-party payment tools, and there is no room for aggregation payment.

Internet of Things payment will become a new outlet for the industry

As far as third-party payments are concerned, in the face of the awakening of giants such as banks, it is meaningless to face positive hardships. Only differentiated and disruptive major innovations can break through. In my opinion, IoT payments can be overwhelming.

The popularity of smart phones has made mobile phones the main carrier of third-party payment, driving the third-party payment industry to open the first wave of prosperity. With the gradual maturity and popularization of Internet of Things technology, the payment field is expected to enter a new stage of “everything is a carrierâ€. Smart bracelets, watches, automobiles, air purifiers, refrigerators, air conditioners, televisions, etc. can all become payment “account carriersâ€. "and "receiving terminals." As an important manifestation of electronic money, payment and clearing realizes digitization and virtualization in a wider range, leading the industry to a new level.

For the third-party payment industry, grasping the opportunity of the great development of Internet of Things payment, we can continue to lead the market in the competition with traditional banks and continue to enjoy the dividends of market pioneers.

According to the research of the major medical, it continues to remind people that a sedentary lifestyle is closely related to many health risks, such as heart disease,back or neck pain, high blood pressure, and obesity.

we have been adhering to the business philosophy of "customer first, quality first" to this day, insisting on providing our customers with high-quality services and high-quality electric Height Adjustable Table and pneumatic lifting desk. Expand our product categories to meet the different needs of customers.

Adjustable Computer Desk,Office Standing Adjustable Desk,Hand Crank Standing Desk,Adjustable Height Office Standing Desks

CHEX Electric Standing Desk , https://www.sjqxhdesk.com